Attending college or university is an exciting time for students, but it can also be financially challenging. With the average student loan debt reaching thousands of pounds, it’s crucial to understand how to avoid excessive debt and manage your money effectively. In this comprehensive guide, we will provide students with essential strategies and tips for avoiding student debt and exploring alternative financing options.

We will explore financial planning for college, including budgeting for education expenses, understanding student debt, and maximizing college savings plans. We will also delve into scholarship and grant opportunities, student loan alternatives, and proactive money management strategies. By taking a proactive approach to financial planning, you can pursue your education goals without incurring unnecessary debt.

Key Takeaways

- Plan ahead and create a realistic budget for education expenses

- Explore scholarship and grant opportunities to secure free money for college

- Consider alternative financing options, such as part-time jobs and employer-funded education

- Maximize college savings plans, such as 529 plans and education savings accounts

- Develop financial literacy skills and seek professional financial guidance when necessary

Understanding Student Debt and Its Consequences

When pursuing higher education, many students turn to loans as a means of financing their studies. However, it’s essential to understand the consequences of taking on debt and to explore ways to prevent it.

Student loan debt can have a severe impact on a student’s financial future. Graduating with significant debt can limit your future financial opportunities and cause undue stress and anxiety. By taking proactive steps to prevent student debt, you can avoid these negative consequences and focus on achieving your goals.

Ways to Avoid Student Debt

- Maximizing scholarship and grant opportunities

- Exploring alternatives to student loans, such as part-time jobs or employer-funded education

- Planning ahead with college savings plans

Student Loan Debt Prevention

Avoiding student loan debt requires careful planning and financial management. It’s crucial to create a realistic budget and stick to it, reducing unnecessary expenses and prioritizing education-related costs. Developing financial literacy skills can also help you make informed decisions and identify potential risks before they become problems.

If you do need to take out student loans, it’s essential to explore repayment options to minimize long-term debt. Strategies such as income-driven repayment plans or loan forgiveness programs can help you reduce your debt burden and achieve financial independence more quickly.

By understanding the consequences of student debt and taking proactive steps to prevent it, you can pursue your education goals without sacrificing your financial future.

Scholarships and Grants: Free Money for College

One of the most effective ways to avoid student debt is by exploring scholarship and grant opportunities. These financial aid resources can provide students with free money for college, reducing the need for student loans and contributing to a debt-free education.

There are numerous scholarships and grants available to students, with some awards covering the entire cost of tuition. To maximize your chances of securing these opportunities, it’s important to understand the options available and develop a solid application strategy.

Sources of Financial Aid Resources

There are multiple sources of financial aid resources available to students, including:

| Source | Description |

|---|---|

| Government | Government grants, such as the Federal Pell Grant, are awarded based on financial need and do not require repayment. |

| Schools | Many colleges and universities provide scholarships and grants to students based on merit, talent, or financial need. |

| Private Organizations | Private organizations, such as businesses and foundations, offer scholarships and grants to students who meet specific criteria, such as academic achievement or community service. |

Maximizing Scholarship and Grant Opportunities

When applying for scholarships and grants, it’s essential to take a strategic approach to maximize your chances of success:

- Research: Research potential scholarships and grants thoroughly, and prioritize those that align with your personal and academic goals.

- Eligibility: Pay close attention to eligibility requirements, ensuring you meet all criteria before applying.

- Deadlines: Keep track of application deadlines, and submit your applications well in advance to avoid missing out on opportunities.

- Quality: Put effort into creating high-quality applications, including well-written essays and polished resumes.

- Follow Up: After submitting your application, follow up with the scholarship or grant provider to ensure they received all required materials and to express your continued interest.

By approaching the scholarship and grant application process with a strategic mindset, students can greatly increase their chances of securing free money for college and pursuing a debt-free education.

Financial Planning: Budgeting for Education

Financial literacy for students is critical for avoiding excessive student debt. One of the most effective ways to stay on top of your finances is by creating a realistic budget for education expenses. Here are some essential budgeting tips to help you manage your finances while pursuing your education goals:

- Evaluate Your Income and Expenses: Start by assessing your income, including any financial aid, scholarships, grants, part-time jobs, or work-study programs. Then, list out all of your monthly expenses, such as rent, utilities, textbooks, transportation, and food. This will give you a clear idea of how much money you have coming in and going out each month.

- Create a Realistic Budget: Based on your income and expenses, create a budget that allows you to cover your basic needs while still leaving room for discretionary spending. Be sure to include an emergency fund in case unexpected expenses arise.

- Track Your Spending: Keeping track of your spending is crucial for staying within your budget. You can use apps, spreadsheets or online tools to monitor your expenses and make adjustments as necessary.

- Reduce Unnecessary Expenses: Look for ways to cut back on unnecessary expenses, such as eating out or buying new clothes frequently. Brown-bagging your lunch and shopping for second-hand items are just a few ways to save money.

- Be Mindful of Credit: Credit can be a useful tool, but it’s important to use it responsibly. Avoid overspending on credit cards or taking out loans that you can’t afford to repay.

By developing a solid financial plan and budgeting for education expenses, you can avoid excessive student debt and make informed financial decisions. Remember, financial literacy for students can lead to long-term financial success.

Exploring Student Loan Alternatives

Although student loans are a common financial aid option for college students, they can put a heavy burden on your finances after graduation. That’s why it’s important to explore alternative methods of funding your education.

One option is to consider a part-time job or work-study program. These options not only provide you with a source of income to pay for tuition, but they also allow you to gain valuable work experience and expand your professional network. Plus, working while studying can help you develop time-management skills which will be beneficial in your future career.

Another alternative is to explore employer-funded education. Some companies offer tuition reimbursement programs to employees who wish to pursue further education. This can be a great way to reduce your student loan debt while gaining the knowledge and skills needed to advance your career.

Additionally, you may also want to consider community college as a cost-effective alternative to four-year universities. Community colleges offer quality education at a fraction of the cost of traditional universities. After completing general education courses, you can then transfer to a four-year university to complete your degree.

Examples of Student Loan Alternatives:

| Alternative | Pros | Cons |

|---|---|---|

| Part-time job or work-study program | Provides income, work experience, time-management skills | May impact study time, limited income potential |

| Employer-funded education | Reduces student loan debt, advances career | May require partnership with employer, may have stipulations |

| Community college | Cost-effective, quality education, transferable credits | May not offer desired degree, limited campus life |

No matter what alternative you choose, it’s important to manage your finances wisely. Create a budget, track your expenses, and look for ways to minimize unnecessary costs. By taking a proactive approach to managing your finances, you can reduce your reliance on student loans and minimize your debt after graduation.

Maximising College Savings Plans

Planning for college expenses can be overwhelming, but the good news is that there are several ways to reduce the burden of student loan debt. One of the most effective methods is to utilise college savings plans. These plans let you earn tax-free interest on contributions, helping your savings grow more rapidly. In this section, we will discuss different savings vehicles and offer tips for maximising your college savings.

529 Plans

A 529 plan is a savings plan designed to help families pay for future education expenses. These plans are sponsored by states, state agencies, or educational institutions, and allow tax-free withdrawals for qualifying expenses, such as tuition, room and board, and textbooks. Some states offer tax deductions or credits for 529 plan contributions, further incentivising savings.

There are two types of 529 plans: prepaid tuition plans and education savings plans. Prepaid tuition plans let you pre-pay tuition at current rates for future college expenses, while education savings plans allow you to save money for future tuition, room and board, and other expenses. Education savings plans generally offer more flexibility, allowing you to choose how to invest your money and potentially achieve higher returns.

When choosing a 529 plan, it’s important to consider fees, investment options, and performance history. You should also assess your risk tolerance and long-term savings goals. Many financial advisors recommend starting a 529 plan as early as possible to maximise the benefits of tax-free growth.

Education Savings Accounts

An education savings account (ESA), also known as a Coverdell ESA, is a tax-advantaged account designed to save for education expenses. Like 529 plans, ESAs allow tax-free withdrawals for qualifying expenses. The main difference between the two is that ESAs can be used for K-12 as well as college expenses, while 529 plans are only for college expenses.

ESAs have contribution limits of $2,000 per year per beneficiary, which can be used for expenses such as tuition, books, and supplies. ESAs offer more flexibility than 529 plans, allowing you to choose how to invest your money, and potentially achieve higher returns. However, it’s important to note that ESAs are only available to families with incomes below a certain threshold.

Maximising Your Savings

While college savings plans can be a powerful tool for reducing student loan debt, it’s important to use them effectively. Here are some tips for maximising your savings:

- Start early: The earlier you start saving, the more time your money has to grow.

- Set goals: Create a savings plan that aligns with your long-term education goals.

- Automate savings: Set up automatic contributions to your savings plan, so you don’t have to remember to save each month.

- Save consistently: Even small contributions can add up over time, so make saving a habit.

- Assess your investment options: Choose investments that align with your risk tolerance and long-term goals.

By following these tips, you can maximise the benefits of college savings plans and reduce your reliance on student loans.

S7: Financial Aid: Navigating the Application Process

Applying for financial aid can be overwhelming, but it’s an essential step in accessing resources to help make your education goals a reality. With a little preparation and the right resources, you can successfully navigate the application process and secure the best possible aid package.

Understanding the Different Types of Financial Aid Resources

Financial aid resources can come in various forms, such as grants, scholarships, work-study programs, and loans. Grants and scholarships are typically free money that does not require repayment, while work-study programs provide part-time employment to help cover educational expenses. Loans, on the other hand, must be repaid with interest. It’s important to fully understand the terms and conditions of any aid offered to make informed decisions.

Completing the FAFSA

The Free Application for Federal Student Aid (FAFSA) is a crucial step in applying for financial aid. It’s important to complete the FAFSA as soon as possible after it becomes available on October 1st each year, as aid is often awarded on a first-come, first-served basis. To complete the FAFSA, you will need to provide information about your financial situation and your family’s income. The FAFSA is used to determine your eligibility for federal aid, as well as state and institutional aid.

Common Mistakes to Avoid

There are several common mistakes students make when applying for financial aid. These include missing deadlines, providing incorrect information, and failing to update information when necessary. To avoid these mistakes, start the application process early, double-check all information before submitting, and make sure to update any changes in your financial situation promptly.

Maximizing Your Aid Package

There are several strategies you can use to maximize your financial aid package. First, be sure to explore all available resources, including federal, state, and institutional aid, as well as outside scholarships and grants. Next, be sure to complete the FAFSA accurately and on time. Finally, consider applying for aid from multiple schools to compare aid packages and negotiate for more favorable terms.

Student Loan Tips

If you do need to take out student loans, it’s important to understand the terms and conditions of the loan before borrowing. Be sure to read the fine print, including the interest rate, repayment terms, and any fees associated with the loan. Consider borrowing only what you need and exploring alternative funding sources before turning to loans.

“Applying for financial aid can seem daunting, but it’s an essential step in accessing the resources you need to achieve your educational goals. With careful planning and attention to detail, you can successfully navigate the application process and secure the aid you need.”

Cultivating Financial Literacy in College

Developing financial literacy skills is essential for long-term financial success. However, many students feel unprepared when it comes to managing finances in college. By taking proactive steps to cultivate financial literacy, you can build a strong foundation for financial independence and avoid excessive student debt.

Understanding Credit

One of the fundamental components of financial literacy is understanding credit. Without a solid grasp of credit, you may find it challenging to navigate loans, credit cards, and other financial products effectively. Here are some tips to help you cultivate credit knowledge:

| Tip | Description |

|---|---|

| Check Your Credit Score Regularly | Knowing your credit score is crucial for securing loans, credit cards, and other financial products. Regularly checking your credit score can also alert you to any errors or inaccuracies. |

| Use Credit Cards Responsibly | Credit cards can be helpful for building credit, but they can also lead to debt if used irresponsibly. To avoid excessive debt, only use credit cards for essential purchases and pay off the balance in full each month. |

| Avoid Opening Too Many Credit Accounts | Opening too many credit accounts can hurt your credit score and lead to excessive debt. Only open accounts that you need and can manage responsibly. |

Managing Student Loans Responsibly

If you need to take out student loans to finance your education, it’s crucial to manage them responsibly. Here are some tips for responsible student loan management:

- Only Borrow What You Need: Before taking out a student loan, carefully consider your expenses and only borrow what you need.

- Keep Track of Repayment Terms: Make sure to understand the terms of your student loan repayment, including interest rates, monthly payment amounts, and repayment period.

- Explore Repayment Options: If you’re struggling to make payments, look into alternative repayment options, such as income-driven repayment plans or loan forgiveness programs.

Building a Strong Foundation for Financial Independence

Finally, to cultivate long-term financial literacy, it’s essential to build a strong foundation for financial independence. Here are some strategies to consider:

- Create a Budget: Track your income and expenses to create a realistic monthly budget.

- Build an Emergency Fund: Aim to save three to six months’ worth of expenses in an emergency fund to protect yourself from unexpected financial setbacks.

- Invest in Your Future: Consider starting an IRA or other retirement account to invest in your future financial security.

By following these tips and strategies, you can cultivate financial literacy and build a strong foundation for long-term financial success. Remember, developing good financial habits now can have a significant impact on your financial future.

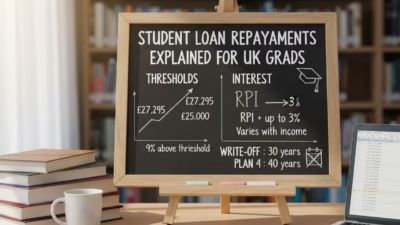

Exploring Student Loan Repayment Options

After graduation, the reality of paying back student loans sets in, and it can be overwhelming. However, you have several options to reduce your student loan debt and manage repayment.

Loan Forgiveness Programs

If you work in certain fields or industries, you may be eligible for loan forgiveness programs. These programs typically require you to work in a specific profession for a set period while making payments on your loans. Some of the common fields that offer loan forgiveness programs include:

| Field/Profession | Program Name | Details |

|---|---|---|

| Education | Teacher loan forgiveness | Federal program that forgives up to $17,500 in loans for qualified teachers |

| Public Service | Public Service Loan Forgiveness | Federal program that forgives remaining loan balance after 120 qualifying payments while working for qualified public service organizations |

| Healthcare | National Health Service Corps Loan Repayment Program | Federal program that repays up to $50,000 in loans for qualified healthcare professionals who commit to working in underserved communities for at least two years |

Explore loan forgiveness programs to see if you qualify and can reduce your student loan debt.

Income-Driven Repayment Plans

If your current income cannot support your monthly loan payments, income-driven repayment plans may be a good option. These plans calculate your monthly payments based on your income and family size. You may even be eligible for loan forgiveness after making payments for a designated period, typically 20-25 years.

Efficient Repayment Strategies

Here are some tips to help you manage and pay off your student loans:

- Pay more than the minimum monthly payment to pay off your loans faster and save on interest charges

- Set up automatic payments to avoid missing deadlines and incurring late fees

- Apply for loan consolidation to simplify payments and potentially lower your interest rate

- Refinance your loans to potentially lower your interest rate and monthly payments

By exploring loan forgiveness programs, income-driven repayment plans, and efficient repayment strategies, you can reduce your student loan debt and manage your loans responsibly. Seek guidance from professionals and stay proactive in managing your finances to build a secure financial future.

Proactive Money Management Strategies

Managing finances in college can be challenging, but with the right approach, it’s possible to stay on top of your money and avoid unnecessary debt. Here are some proactive money management strategies to consider:

Create a Realistic Budget

The first step in effective money management is creating a budget. This allows you to track your expenses and income and make informed financial decisions. A realistic budget should include all your expenses, including housing, food, transportation, tuition fees, textbooks, and other essential items. Use budgeting apps or templates to help you track your expenses and identify areas where you can cut back.

Reduce Unnecessary Expenses

Reducing unnecessary expenses is a great way to save money and avoid debt. Consider purchasing used textbooks instead of new ones, using public transportation instead of owning a car, and looking for free or low-cost activities instead of expensive entertainment. Small changes can add up and make a big difference in your finances.

Avoid Credit Card Debt

Credit cards can be useful for building credit, but they can also lead to debt if not used responsibly. Avoid using credit cards for everyday purchases, and only use them for emergencies or when you can pay off the balance in full each month. High-interest rates on credit cards can quickly spiral out of control, leading to unmanageable debt.

Seek Financial Assistance

If you’re struggling to manage your finances, don’t hesitate to seek financial assistance. Many colleges offer financial planning services or workshops to help students understand budgeting, loans, and credit. You can also seek guidance from a financial advisor or student loan counselor to help you navigate your finances and avoid debt.

Stay Organized

Staying organized can help you stay on top of your finances and avoid missed payments or late fees. Keep track of all your bills and due dates, and set reminders for when payments are due. Create a filing system for important documents, such as financial aid paperwork or loan statements, so you can easily find them when needed.

By following these proactive money management strategies, you can stay on top of your finances while pursuing your education goals. Remember, financial literacy is key to avoiding student debt and building a strong foundation for your future.

Seeking Professional Financial Guidance

While the tips and strategies outlined in this guide can help students manage their finances and avoid student debt, seeking professional financial guidance can provide additional support and expertise.

Financial planning for college can be complex, and a financial advisor can provide tailored advice to help you meet your unique goals. They can help you create a realistic budget, develop a savings plan, and explore various funding options, including scholarships, grants, and loans.

Additionally, student loan counselors can offer valuable advice and resources for managing student loans, including repayment options and loan forgiveness programs. These professionals can also provide guidance on consolidating loans, negotiating with lenders, and managing other debt obligations.

Student Loan Tips from Professionals

- Schedule regular meetings with a financial advisor or counselor to stay on top of your finances and develop a long-term financial plan.

- Research potential advisors and counselors carefully to ensure that they have experience working with college students and understand the unique challenges of managing finances during this time.

- Be open and honest about your financial situation and goals, so that your advisor can provide targeted advice and support.

- Take advantage of all available resources, including online tools, workshops, and seminars, to build your financial literacy and stay informed about new developments in college funding and financial planning.

- Don’t be afraid to ask questions or seek clarification when discussing complex financial topics. Your advisor is there to help you, and you should feel comfortable addressing any concerns or uncertainties you may have.

Ultimately, seeking professional financial guidance can be a crucial step in building a strong financial foundation and avoiding excessive student debt. By working with experienced advisors and counselors, you can develop a comprehensive financial plan that aligns with your education goals and sets you up for long-term success.

The Student’s Playbook for Avoiding Student Debt and Managing Money

In this comprehensive guide, we will provide students with essential strategies and tips for avoiding student debt. We will also explore effective ways to manage money while pursuing your education goals.

Understanding Student Debt and Its Consequences

Before delving into strategies for avoiding student debt, it’s important to understand the consequences it can have on your financial future. In this section, we will discuss the basics of student debt, its impact, and why it’s crucial to take proactive steps to prevent it.

Scholarships and Grants: Free Money for College

One of the most effective ways to avoid student debt is by exploring scholarship and grant opportunities. We will explore different types of financial aid resources available to students and provide tips on how to maximise your chances of securing free money for college.

Financial Planning: Budgeting for Education

A solid financial plan is key to avoiding excessive student debt. In this section, we will discuss the importance of financial literacy and budgeting for education expenses. Learn how to create a realistic budget and make informed financial decisions.

Exploring Student Loan Alternatives

While student loans are often seen as the go-to option for financing education, there are alternatives worth considering. We will explore different options, such as part-time jobs, work-study programmes, and employer-funded education, to help you minimize reliance on loans.

Maximising College Savings Plans

Planning ahead and utilising college savings plans can significantly reduce the need for student loans. We will discuss different savings vehicles, such as 529 plans and education savings accounts, and provide tips on maximising your savings for college.

Financial Aid: Navigating the Application Process

Applying for financial aid can be overwhelming, but it’s essential to access available resources. In this section, we will guide you through the financial aid application process, highlight common mistakes to avoid, and offer tips for securing the best possible aid package.

Cultivating Financial Literacy in College

Developing financial literacy skills is crucial for long-term financial success. We will explore ways to cultivate financial literacy during your college years, including understanding credit, managing student loans responsibly, and building a strong foundation for financial independence.

Exploring Student Loan Repayment Options

Even with careful planning, some students may still need to take out student loans. We will discuss various repayment options, including loan forgiveness programmes, income-driven repayment plans, and strategies for paying off loans efficiently.

Proactive Money Management Strategies

In this section, we will delve into practical money management strategies for students. From creating a monthly budget to reducing unnecessary expenses, you’ll discover effective ways to stay on top of your finances and avoid unnecessary debt.

Seeking Professional Financial Guidance

Sometimes, seeking professional advice can make a significant difference in managing your finances and avoiding student debt. We will discuss when and where to seek guidance, including financial advisors, student loan counsellors, and other helpful resources.

Conclusion

In conclusion, by following the strategies and tips outlined in this guide, students can empower themselves to avoid excessive student debt and manage their money effectively. With careful planning, financial literacy, and exploring alternative funding options, you can pursue your education goals without burdensome loans.

FAQ

How can I avoid student debt?

There are several strategies you can use to avoid student debt, such as applying for scholarships and grants, exploring student loan alternatives like part-time jobs and work-study programs, and maximizing college savings plans.

What are the consequences of student debt?

Student debt can have long-term consequences on your financial future, including impacting your ability to qualify for loans or mortgages, delaying major life milestones like buying a house or starting a family, and causing financial stress and mental health issues.

How can I find scholarships and grants?

There are various financial aid resources available to students, including scholarship search engines, college financial aid offices, and community organizations. It’s important to research and apply for scholarships and grants that match your qualifications and interests.

How do I create a budget for education expenses?

Financial planning is crucial for managing education expenses. Start by identifying your income sources and listing your expenses. Prioritize your needs and allocate funds accordingly. Regularly review and adjust your budget as needed.

What are some student loan alternatives?

Instead of solely relying on student loans, consider other options like part-time jobs, work-study programs, employer-funded education, or attending community college before transferring to a four-year institution. These alternatives can help reduce your reliance on loans.

What are college savings plans?

College savings plans, such as 529 plans and education savings accounts, are tax-advantaged accounts designed to help families save for education expenses. By contributing regularly to these plans, you can accumulate funds to cover tuition, books, and other college costs.

How do I apply for financial aid?

To apply for financial aid, complete and submit the Free Application for Federal Student Aid (FAFSA) online. Be sure to gather all necessary documents and meet deadlines. Additionally, research and apply for any additional scholarship or grant opportunities specific to your college or state.

How can I improve my financial literacy in college?

Take advantage of resources like personal finance courses, workshops, and online tools to enhance your financial literacy. Learn about credit management, responsible borrowing, and investing. Implement good financial habits early on to set yourself up for success.

What are some student loan repayment options?

There are various repayment options available, such as income-driven repayment plans, loan forgiveness programs for certain professions or public service, and refinancing options. It’s important to explore these options and choose the one that best fits your financial situation.

How can I manage my finances effectively in college?

You can manage your finances effectively in college by creating a monthly budget, tracking your expenses, prioritizing needs over wants, and seeking ways to reduce unnecessary expenses. It’s also helpful to educate yourself on financial resources available on campus.

When should I seek professional financial guidance?

If you’re feeling overwhelmed or unsure about your financial situation, it may be beneficial to seek professional financial guidance. Consider reaching out to financial advisors, student loan counselors, or other resources provided by your college or community.