Rent’s due, your loan hasn’t landed (or it’s smaller than you planned), and your bank balance is doing that horrible slow blink. If you’re studying in the UK, a university hardship fund can be the thing that keeps you on your course when money problems hit hard and fast.

Hardship funds aren’t “free money for everyone”. They’re more like a campus fire extinguisher, there for sudden financial emergencies, not to heat the whole building all winter. The good news is that if you apply with the right evidence and a clear explanation, you give yourself a real chance.

Key Takeaways

- A university financial assistance fund, usually called a hardship fund, is a non-repayable grant meant to help mitigate financial hardship from short-term financial shocks.

- Most universities expect you to show you’ve applied for your maintenance loan and other support you’re eligible for.

- You’ll almost always need recent bank statements, proof of rent or bills, and evidence of what changed.

- Decisions are discretionary, and funds are limited, so applying early matters.

- A short, factual statement (plus a simple budget) often works better than a long emotional one.

Table of Contents

- Key Takeaways

- What A University Hardship Fund Is (And What It Can Cover)

- Who Can Apply In 2026 (And Who Often Gets Priority)

- What Proof You Need For A Hardship Fund Application (And How To Avoid Rejection)

- Copy-Paste Statement Template For Your Hardship Fund Application (2025-2026)

- Frequently Asked Questions About University Hardship Funds In The UK

- Conclusion

What A University Hardship Fund Is (And What It Can Cover)

A university hardship fund, or financial assistance fund, is financial support offered by your university when you’re struggling to meet essential participation costs. It’s normally aimed at helping you stay enrolled, keep up with study, and complete your study programme, rather than fixing long-term underfunding.

Most hardship support from a financial assistance fund is paid as a cash award, which means you don’t pay it back. Some universities may offer cash awards in other forms too, such as food vouchers or additional food vouchers, or other forms of in-kind student support like help with specific urgent costs. The exact rules vary, and the fund can run out, so it’s always worth checking your own university’s guidance and applying as soon as you can to ensure you can complete your study programme.

Hardship funding commonly helps with essentials like:

- rent arrears (or preventing arrears)

- utility bills and basic living costs

- travel costs that are unavoidable (for example, placement travel)

- emergency replacement costs (for example, a stolen phone needed for contact and banking)

- childcare costs that block you from attending

What it usually won’t cover is “normal” student overspending, lifestyle costs, or predictable gaps you could’ve planned for. If you want a student-friendly overview of how hardship funds tend to work across UK universities, hardship funds explained for students{:rel=”nofollow” target=”_blank”} is useful context.

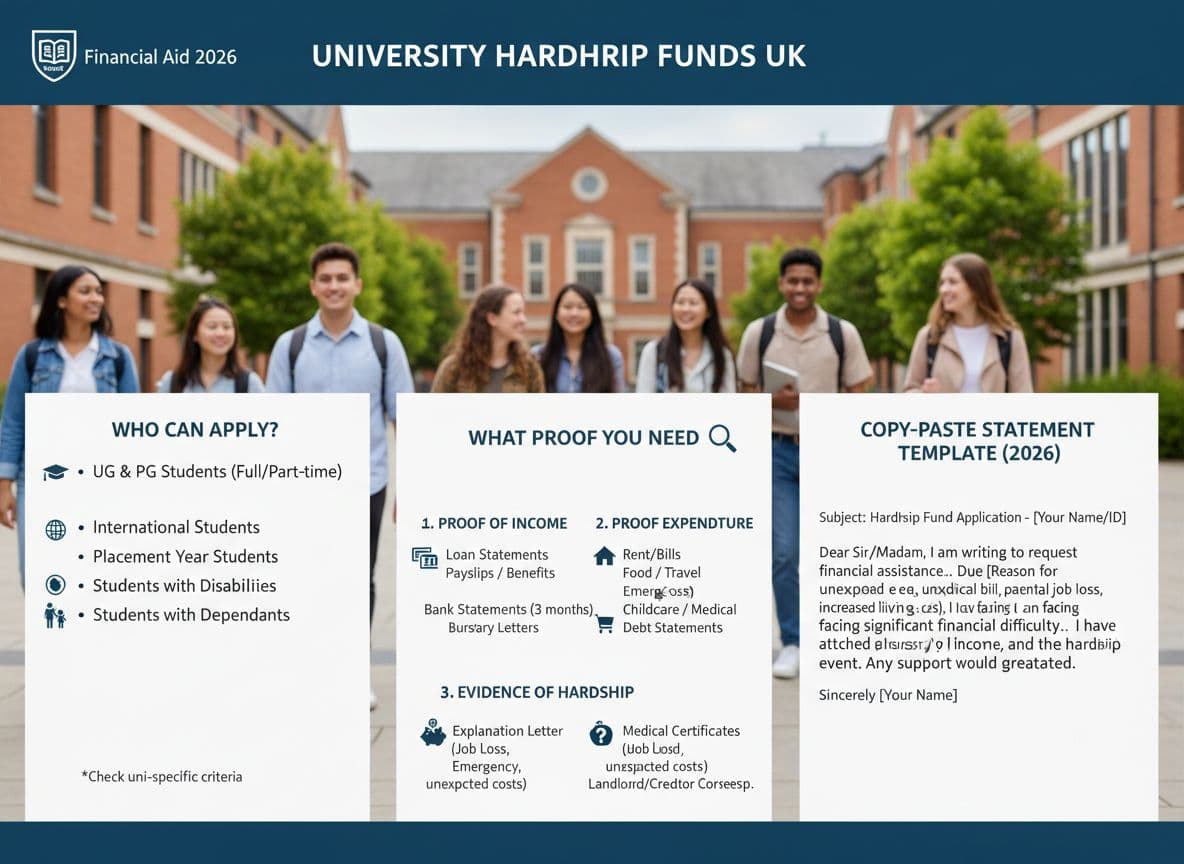

Who Can Apply In 2026 (And Who Often Gets Priority)

In the academic year 2025 to 2026, most UK universities apply specific eligibility criteria and residency criteria for hardship funding, restricting it primarily to current, enrolled students (undergraduate or postgraduate). Many accept applications from full-time and part-time students regardless of their study programme, but you’ll need to demonstrate that your financial situation changed due to an unexpected or unavoidable event while meeting the residency criteria.

Common situations that meet the eligibility criteria include sudden job loss, illness preventing work, loss of family support, relationship breakdown impacting housing costs, or urgent expenses like travel for a family emergency.

Universities also tend to prioritise defined vulnerable groups when funds are tight. That often includes care leavers, estranged students, student parents, disabled students, and students with caring duties within these defined vulnerable groups. Care leavers, in particular, receive strong priority among defined vulnerable groups. Some universities have separate routes for international students, sometimes with different limits or rules, and support remains available regardless of study programme for defined vulnerable groups. For example, you can see how one university frames its criteria on the Oxford Assistance Fund page{:rel=”nofollow” target=”_blank”}.

One thing that surprises students is that universities may expect you to have taken reasonable steps first, like applying for the right student finance, checking benefit eligibility, and reducing non-essential spending, regardless of your study programme. If you’re not sure you’ve done the basics (or you keep getting stuck on forms), this internal guide is handy: UK student finance application checklist.

What Proof You Need For A Hardship Fund Application (And How To Avoid Rejection)

Think of your application form like a short story with receipts. Your university needs to see (1) what you normally have coming in, (2) what’s going out, and (3) what changed. To verify your actual financial need, they conduct a household income assessment and an individual assessment of need.

Most hardship applications ask for recent bank statements, often covering the last 2 to 3 months for your study programme. They also tend to ask for supporting documents of your main costs and your income. If you’re missing supporting documents, your application can stall or be rejected, even if your situation is serious.

Here’s what’s commonly requested:

- Bank statements for all accounts you use (including overdrafts)

- Tenancy agreement and rent schedule, or proof of housing costs if in halls

- Bills (utilities, council tax if applicable, phone contract)

- Income proof (payslips, student finance entitlement, bursary letters, Universal Credit award notice, disability living allowance, Personal Independence Payments, benefits screenshots)

- Evidence of the problem (GP note, fit note, employer letter, redundancy email, fraud report, repair invoice)

- A basic budget breakdown (many universities use a template)

These supporting documents, required for the academic year 2025 to 2026, help with a household income assessment and individual assessment of need to confirm actual financial need specific to your study programme. For instance, include Universal Credit award notices, disability living allowance details, and Personal Independence Payments as relevant income proof.

Two avoidable mistakes cause loads of delays. First, sending blurry screenshots where dates and names can’t be read on bank statements or supporting documents. Second, not explaining unusual transactions (for example, a one-off transfer from family last month that doesn’t exist now). Add one sentence to clarify, and it saves back-and-forth.

If your budget doesn’t exist yet, don’t panic. Build a simple monthly plan first, then attach it. This internal guide can help you sanity-check realistic costs: first-year uni student budget UK.

For a clear example of the sort of documents and steps a university may list, see the University of Bristol’s financial assistance fund guidance{:rel=”nofollow” target=”_blank”}.

Copy-Paste Statement Template For Your Hardship Fund Application (2025-2026)

Eligible students facing financial hardship during the academic year 2025 to 2026 should use this copy-paste template as a starting point for their application. It provides a clear format for eligible students experiencing financial hardship. Then edit the bracketed parts to match your situation. Keep it factual, calm, and specific.

Hardship Fund Statement (2025-2026)

I’m a registered student on [study programme] in [year of study]. I’m applying for hardship support because I’m currently unable to meet essential living costs due to [what changed, for example: loss of part-time job / illness / unexpected housing cost].My current monthly income is £[amount] from [student finance / wages / benefits / family support]. My essential monthly costs are £[amount] (rent £[x], bills £[x], food £[x], travel £[x]). This leaves a shortfall of £[amount] per month.

The hardship started on [date]. The main reason is [one or two sentences explaining the cause]. I’ve attached evidence of this, including [bank statements / tenancy agreement / medical note / employer letter].

I’ve taken steps to improve my situation by [what you’ve done: reduced non-essential spending, applied for extra shifts, spoken to Student Finance, applied for benefits, arranged a payment plan]. Despite this, I’m at risk of [rent arrears / missing essential travel / being unable to afford food].

I’m requesting £[amount] to cover [what it will cover] for the period [dates]. This support would help me stay on my course and continue attending classes.

Frequently Asked Questions About University Hardship Funds In The UK

Do You Have To Pay A University Hardship Fund Back?

Usually no, it’s commonly awarded as a grant or cash award. This university fund differs from post-16 education funding like the 16 to 19 Bursary Fund or a discretionary bursary, which might be managed by a local authority. For example, post-16 education funding through the 16 to 19 Bursary Fund or a discretionary bursary from a local authority often supports students receiving income support during earlier study stages. Some students may also be receiving income support now. Your university will tell you if any part is repayable.

How Long Does A Hardship Fund Decision Take?

Many universities aim for a decision within a few weeks, but it depends on demand and whether your evidence is complete. Missing documents nearly always slow things down.

Can International Students Apply For Hardship Funds?

Sometimes yes for international students, but some universities run a separate international hardship fund with its own rules. Check your university’s funding pages and ask student support if it’s unclear, especially regarding your study programme.

What If My Application Is Rejected?

Ask for the reason, then re-apply if you can fix it (for example, add missing bank statements, clarify spending, or provide stronger evidence). Also ask what other support the university can offer.

Conclusion

A financial assistance fund won’t solve every money problem, but it is a vital resource for defined vulnerable groups, including care leavers. This discretionary bursary can stop a bad month becoming a full-on crisis for these defined vulnerable groups. Apply early to the financial assistance fund, send clean evidence, and make your statement simple and specific if you are part of care leavers or other defined vulnerable groups. If you’re unsure what to include, book a quick appointment with your student money adviser; they can often spot what’s missing in minutes. A cash award from this financial assistance fund, often provided as a discretionary bursary to defined vulnerable groups, can help you stay on your study programme, while another cash award offers similar support.